With soaring inflation and rising interest rates, New Zealand consumers are facing increasing pressure to manage household budgets. In such inflationary times the parallel pressures on marketers to acquire and retain customers is more evident than ever.

Major household expenditures are being put on the backburner, leading to marketers having to decide who to target, new customers or existing customers. With marketing budgets also under pressure, the ratio of spend between the two groups is a key decision.

In hard times, the importance of customer retention makes it worth the investment and many companies and brands are funnelling more money into loyalty schemes and the technology necessitated by these.

“On average, 50 percent of a company’s sales come from the top 20 percent of its customers, not 80 percent,” according to Kevin O’Connell, a Grant Thornton Managing Director in Strategy and Transactions, so in his opinion, marketers should throw out the old 80:20 belief that 80 percent of sales comes from the top 20 percent of customers.

On that basis, marketers need to analyse their sector and their own brands to ensure funds are not wasted. Not all market sectors have the same behaviours, so knowing the returns on acquisition and retention decisions is imperative.

Businesses can’t grow effectively by simply focusing on their top customers. Often, there simply aren’t enough of them. To achieve true growth, companies need to continually increase market penetration.

With changing life stages, today’s frequent customers are not necessarily the frequent customers of tomorrow. On that basis, market penetration has to be the key driver for any brand.

There are three distinct areas that contribute to driving customer growth: Acquisition (attracting new customers), Development (increasing the value of existing customers through upselling and cross-selling), and Retention (keeping existing customers coming back for more).

The link between customer growth and value growth is simply “the more customers you have, the more revenue you can generate, and the more value you provide to your customers, the more likely they are to stay with you and spend more money with you”.

So, how are local marketers creating customer-centric growth strategies to help achieve their business goals?

Telecommunication company Spark, in a New Zealand category-first, recently introduced its Made For You Review (MFYR) programme, which delivers an annual personalised check-in, giving customers insights into their behaviour, checking their plan inclusions to enable right-plan conversations.

This digitally led, human-backed communication strategy, put data-driven insights directly into its customers hands and at the fingertips of Spark frontline teams so as to enrich in-person conversations.

MFYR is the largest and most complex customer communication strategy ever delivered by Spark, which has led to business-wide transformations that have improved customer experiences. The initiative is reported to have delivered a substantial reduction in churn.

This was not a short-term campaign, but an ongoing promise to customers that has driven a commitment to invest effort in long-term solutions.

Spark has always been obsessed with acquisition, but with current market conditions, and in the face of skyrocketing churn, the company saw the need for a dramatic shift from the traditional transactional, product-centric approach of the category to a radically different approach, focused on building trust and value perceptions with every customer individually.

Trust is a key component in both customer retention and new customer acquisition. The 24th Annual Most Trusted Brands survey, as declared by Reader’s Digest, revealed a crucial insight regarding brands: the ability to maintain trust in the face of economic hardships necessitates innovation, adaptability, and most importantly, excellence. The survey of more than 1,000 Kiwi consumers and 100 senior business leaders found a strong correlation between brand trust and consumer behaviour.

Whittaker’s is testament to this, winning Most Trusted Confectionery, Most Trusted New Zealand Iconic Brands and Most Trusted Of All Brands Surveyed. The brand’s success is due to actively engaging with its community of chocolate lovers and integrating their feedback and ideas into its business strategy.

Apart from trust in a brand, the ever-increasing influence of price as a key decision influencer in hard times is of primary importance. PAK’nSAVE’ has defended its lowest price position for many years and this approach is central to the retailer’s ability to retain and attract customers.

Five insights, and strategic conclusions, have formed the basis of PAK’nSAVE’s extraordinarily long, cost-efficient, and successful defence of its leadership position: Promote the sacrifice, look cheap, be loved, make Kiwis proud, and one big lasting idea.

While other supermarkets rightly promote other benefits, such as convenience, range, quality, freshness, store experience and helpful, expert staff, those benefits undermine low-price perceptions because they cost money to deliver. This insight led to PAK’nSAVE’s very bold decision. It told shoppers what they wouldn’t get at PAK’nSAVE. Promoting the small sacrifices that their clever shoppers made would strengthen PAK’nSAVE’s lowest-prices position. That was the sacrifice.

People are suspicious of a low-price retailer with expensive advertising and the now famous, stickman campaign continues to remind shoppers that everything PAK’nSAVE does, including their advertising, helps keep prices down.

The entertaining and popular advertising helps Kiwis feel great, and smart about their choice. In addition, being New Zealand owned and owner-operated, gives each store a special local connection. New Zealanders like to support Kiwi brands that show they understand them. So, the advertising is overtly and humorously Kiwi, and is a big lasting idea.

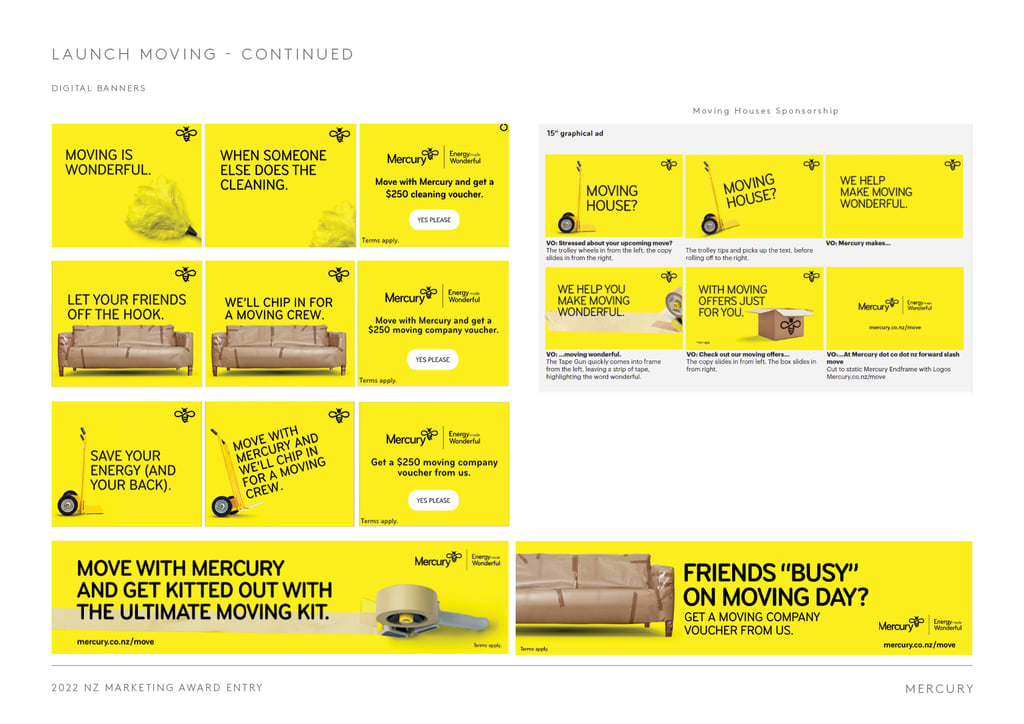

What a brand does is as important as what a brand says, so the customer experience will have to be in-sync with the promise. However, this alone will often merely maintain market share, rather than grow it. Winner of the Excellence in Utilities/Communications Marketing Strategy 2022 at last year’s Marketing Awards, Mercury, saw a potential market in customers moving homes. Mercury decided to tap into the world of moving in order to make up the potential loss of 20,000 customers every month.

Around 67 percent of home movers choose to switch energy providers at this time, providing an opportunity for Mercury to work towards retaining more movers and convert more switchers.

The ‘Mercury Movers’ campaign launched with an offer to clean homes and using data, Mercury was able to split customers between genuine movers and property watchers. They offered $250 off house cleaning and truck rental when customers chose to move with them.

For the first time in five years, Mercury was able to see a positive customer growth, ending the campaign with more than half of acquired movers on contract.

Another local example of acquisition in hard times was the creation by Xero of its content hub with practical tips and resources to educate small and medium businesses with information that would make a significant difference to their business practices.

Increasing the value of existing customers is probably the go-to strategy for those marketers battling to win new customers against more heavily funded competitors. This is the position facing market latecomer 2degrees. A key focus of 2degrees commercial strategy is growing margin through data monetisation. The telco managed to deliver value through its Perks loyalty programme, achieving its key objectives of ARPU (average revenue per unit) growth, loyalty, and churn management.

The marketing team looked at customers’ existing data balances, testing varying thresholds to help determine at what level customers would be most likely to take up the offer. They split customers by plan type and data balance, creating 20 segments to test and learn from. Different data amounts and price points were also tested, and four different offers were selected (based on learning from previous campaigns) to understand the price sensitivity of different segments.

The goal was to test price elasticity, maximising revenue per gigabyte of data, while still delivering real value to customers. Results of the campaign confirmed the assumption that customers with lower data balances would be most likely to convert. What was surprising, was the number of customers with higher data balances who also chose to purchase more data.

Each market sector has its own issues. Insurance companies have traditionally looked to grow by getting customers to switch from other competitors for easy financial wins. Insurance company State, decided to change the paradigm, needing to do something drastically different to reverse its six years of consecutive customer loss.

State discovered through research that the real reason people weren’t buying contents insurance was that they didn’t believe they had enough stuff worth insuring. So, the value people placed on insurance was entirely dependent on the value of their stuff. It also found that under 35s were twice as likely to not have contents insurance.

These insights transformed State’s approach. The insurance provider discovered that it could lead the market in talking to this previously ignored uninsured market, offering them the protection they didn’t know they needed by starting a conversation around the value and benefits of insurance.

State created ‘Tally’, a modern take on an insurance calculator, an online app with Tinder-style swipe functionality that quickly establishes how much an individual’s stuff is worth. It’s fast, free, and available to all (not just State customers). Most importantly, it’s also pre-populated with the most common items that State’s target market might own. It also estimated the value of those items, as a starter, so users didn’t have to figure it out themselves.

People want to engage as little as possible with insurance, but State found a way to help get people the cover they needed, and do it in a quick, more exciting way.

Most businesses are not customer-centric in the development or execution of their growth strategy. Or at the very least, are only scratching the surface in terms of what is now possible. As a result, at a time when marketers are being asked to do more with less, and growth, yield and ROI on marketing spend are critical, they are leaving money on the table.

Not all customers are created equal. and there are even customers who actually cost the business money. Any customer-centric growth strategy should start with an analysis of individual customers, with strategy focusing on the customers who matter most.

Specific strategies for growth will depend on how mature the business is and the nature of the commercial relationship with the customer. Some have high switching barriers, banking being a prime example, while others have a high frequency of transactions, as is the case with grocery.

There is, therefore, no hard and fast rule, to cover all businesses. If the business is still early in its maturity and in high growth mode, then a higher level of investment in acquisition makes sense, while a business that is at a more mature stage can determine acquisition investment based on overall business revenue and profit targets and the gap to close, once revenues from existing customers are factored in.

If the business has a product that is purchased as a one off or has a very long time between purchases, then most of the investment will go to acquisition. Notably these businesses are not necessarily good In the current economic climate, biggest general shift has been from investment allocated to longer term brand building activity to short term ‘performance’ based activity. That’s not surprising given the focus on yield and ROI. The impact of the short-term activity is easier to quantify and measure, even though it’s not necessarily the right strategy.

Aligning investment to expected customer lifetime value and understanding what triggers people into the market is key. Loyalty is an outcome not a programme, so focusing on getting the core customer experience right is the road to success.

Make it easy for customers to do business with you. Be proactive, don’t wait for customers to come to you with problems. Reach out to them regularly to ask for feedback and to see if there’s anything you can do to improve their experience. And show your appreciation. Thank your customers for their business and let them know that you value their loyalty and create a customer experience that will keep your customers coming back for more.